Single and multiple risk factors in the Egyptian stock market

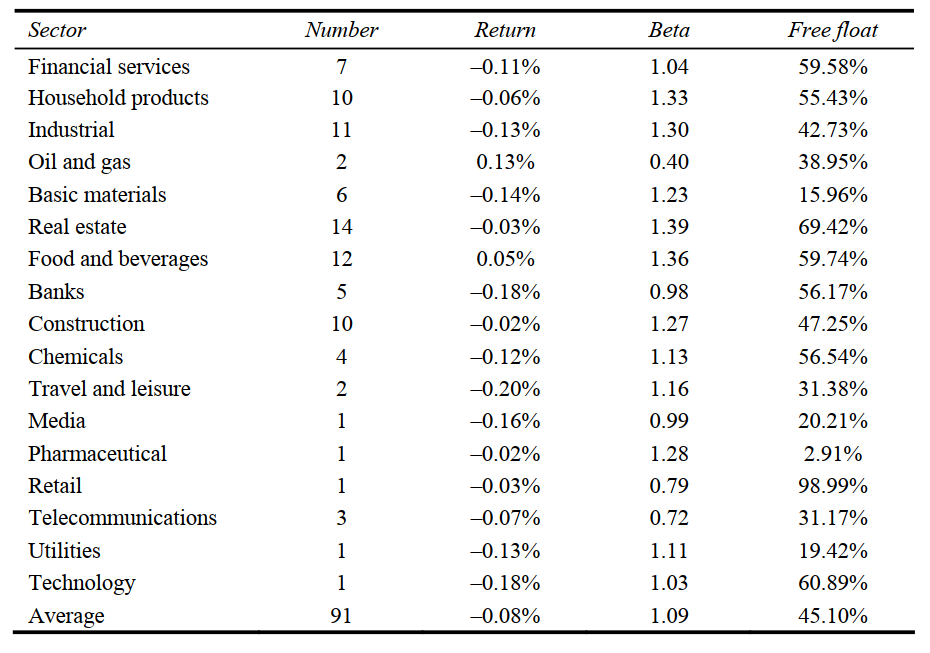

The return-risk trade-off of the 100 stocks contained in the Egyptian EGX100 index is examined. The Egyptian stock market has an average free float of only 45%. It is estimated that 50% of trading in the free float stocks is dominated by large investors, and local and international fund managers. The market suffers from low turnovers and more recently long periods of trade suspension after the political unrest of January 25th, 2011. The study finds that a serial correlated returns model is more suitable to estimate returns for low free float stocks in Egypt. However, it is unlikely that this serial correlation could lead to above average trading profits since it is a reflection of ownership concentration in a small illiquid market. The market offers diversification benefits due to its low correlation with major world indices. However, trade suspension due to political instability is an extra risk that could negate diversification benefits. Copyright © 2013 Inderscience Enterprises Ltd.